In the fall, gold resembles a hot air balloon. It inflated when the armed conflict started in the Middle East. And it started to creak at the seams after investors realized that the war would be of a local nature. It is unlikely to extend beyond Israel and is likely to end soon. Therefore, there can be no talk of oil prices rising above $150 per barrel or precious metals exceeding $2,200 per ounce.

Market veterans note that geopolitical factors are typically short-lived. The onset of armed conflicts in Ukraine and Israel shocked financial markets, but gradually, the global economy and markets adapted. The geopolitical risk premium in the Middle East has completely disappeared from oil prices and is gradually fading from gold. As a result, XAU/USD quotes are falling even against a weakening dollar and declining yields on U.S. Treasury bonds.

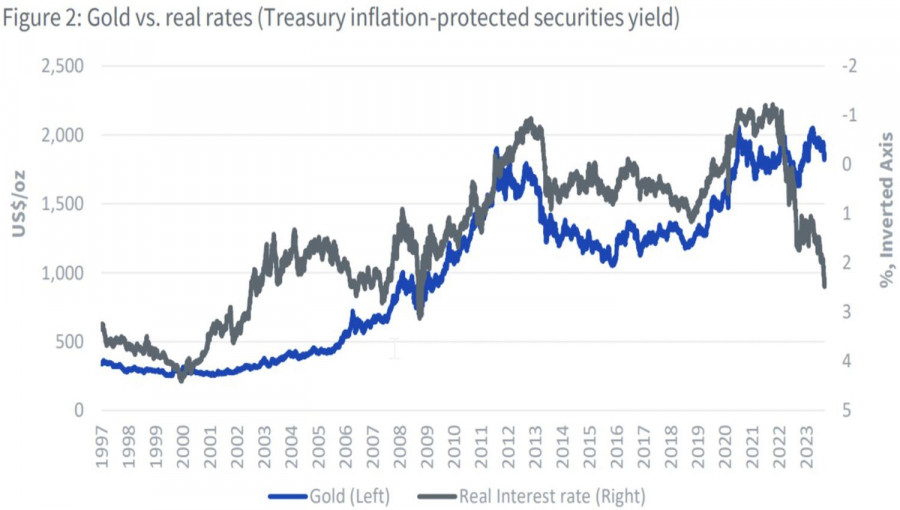

In a calm environment, gold reacts to the Fed's monetary policy. Its tightening usually leads to a decrease in the price of precious metals and vice versa. Thus, the substantial stimulus from the Federal Reserve during the pandemic in 2020 pushed futures quotes to a record high of $2,072. Gold surpassed the $2,000 mark per ounce in 2023 against the backdrop of the U.S. banking system crisis, which increased recession risks and, on paper, should have prompted Fed Chairman Jerome Powell and his colleagues to make a dovish pivot.

Dynamics of Gold and U.S. Treasury Bond Yields

This year, there is a significant discrepancy in the dynamics of XAU/USD and the real yields of U.S. Treasury bonds. This is due to a multitude of events characterized as Black Swans. In addition to the bankruptcies of American banks and the crisis in the Middle East, one can also attribute de-dollarization to them. The shift of central banks away from the U.S. dollar amid the freezing of Russian assets led to record purchases of precious metals by regulators in 2022. The People's Bank of China led and continues to lead this process. In October, it increased its gold reserves by 23 tons to 2,215 tons. Since the beginning of 2023, the indicator has grown by 204 tons.

According to the World Gold Council, a 10% rise in precious metals due to geopolitics is not supported by speculators' desire to acquire it, as well as the increase in the holdings of specialized exchange-traded funds. Gold needs a new driver to move higher, but it doesn't have one at the moment. And there is no smell of an escalation of conflict in the Middle East, as Israel and the U.S. are discussing what Gaza will be like after the destruction of Hamas.

The further fate of XAU/USD will likely depend on American inflation and the Fed. The geopolitical risk premium is gradually disappearing from prices, but after the drop to the $1,935–1,950 per ounce range, investors will take into account the monetary policy. A slowdown in CPI is a reason to go long on precious metals and vice versa.

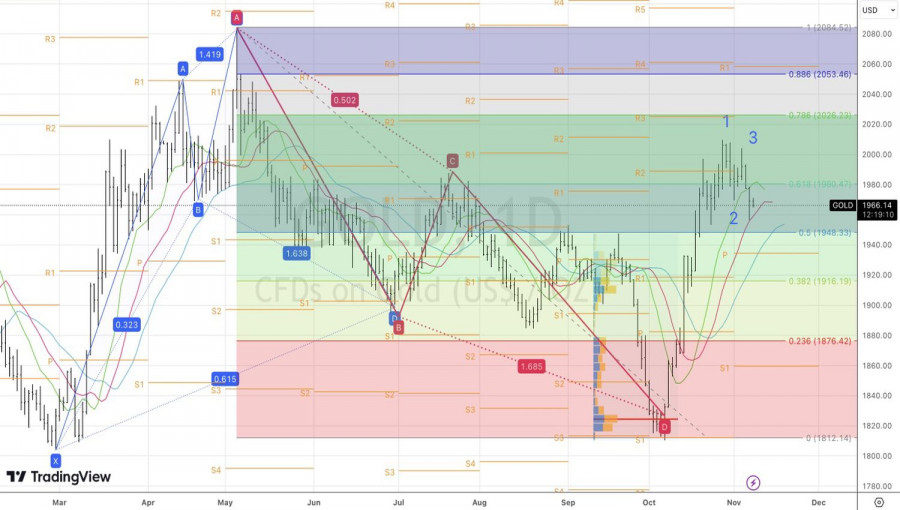

Technically, on the daily chart of gold, there can still be a transformation of the Shark pattern into a 5–0. Therefore, a drop in quotes below $1,950 per ounce is a reason for selling. On the contrary, a rebound from this level will allow buying precious metals.

Download NOW!

Download NOW!

No comments:

Post a Comment