The European Central Bank will hold its monetary policy meeting on Thursday, June 6. Traders are highly confident that the ECB will lower its benchmark deposit rate by 25 basis points, mainly because members of the Governing Council have repeatedly indicated this step in the past.

The main source of optimism that drives the euro higher is that, by several indicators, the manufacturing sector in the Eurozone has started to steadily recover. The balance of orders and inventories reached a 2-year high in May. Labor market tensions are increasing, with employment rising by 0.3% in the first quarter, indicating that the economy continues to create new jobs.

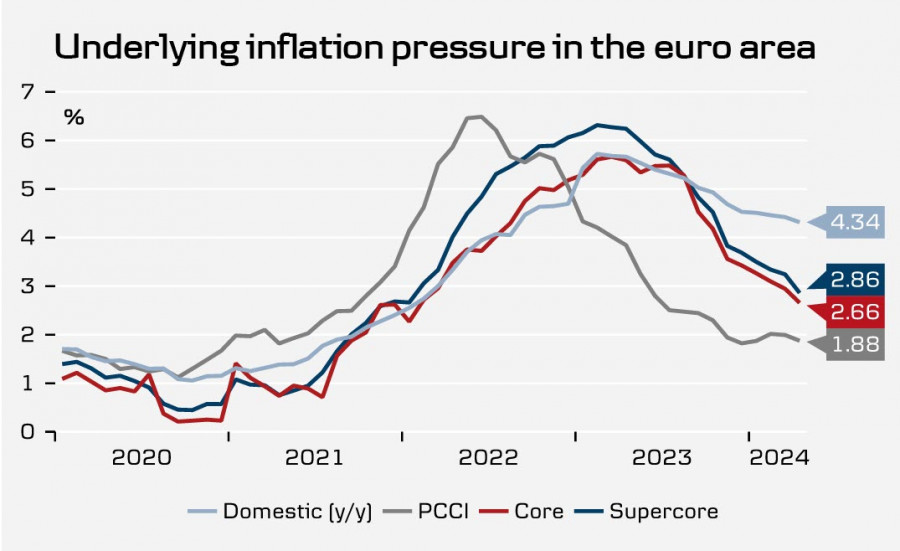

The Eurozone inflation outlook is mixed. The services sector contributed approximately 3.7% year-on-year, and the downward trend is weak, while non-energy industrial goods are growing by only 0.9% y/y. Domestic inflation, meaning non-exportable inflation, is still too high at 4.3%. Its decline appears to be stable, but the pace is slow.

During the March and April ECB meetings, ECB President Christine Lagarde emphasized that by June they would know "much more." Since then the key indicators have shown that activity has unexpectedly increased in April, which continued into May, and a smaller-than-expected decline in inflation. There is a risk that inflation will decrease more slowly than forecasts suggest, meaning the ECB may not cut rates as aggressively as the markets currently expect. If these concerns materialize, the trajectory of rate cuts will become less steep, generally supporting the euro due to the retention of higher yields.

For instance, wage growth was 4.7% in the first quarter, 0.2% higher than the previous quarter. Although the ECB has highlighted that this growth is largely due to base effects, and faster indicators point to a decrease in wages, the risk of the ECB refraining from rate cuts cannot be ignored. Perhaps this is what the markets are considering when they buy the euro.

The potential rate cut is already fully priced in by the market, so the ECB meeting results are unlikely to trigger a euro sell-off. Markets assume that the Eurozone's economic recovery pace exceeds forecasts, so the risks are generally towards a slower rate cut trajectory rather than a faster one, making surprises more likely to favor further euro appreciation.

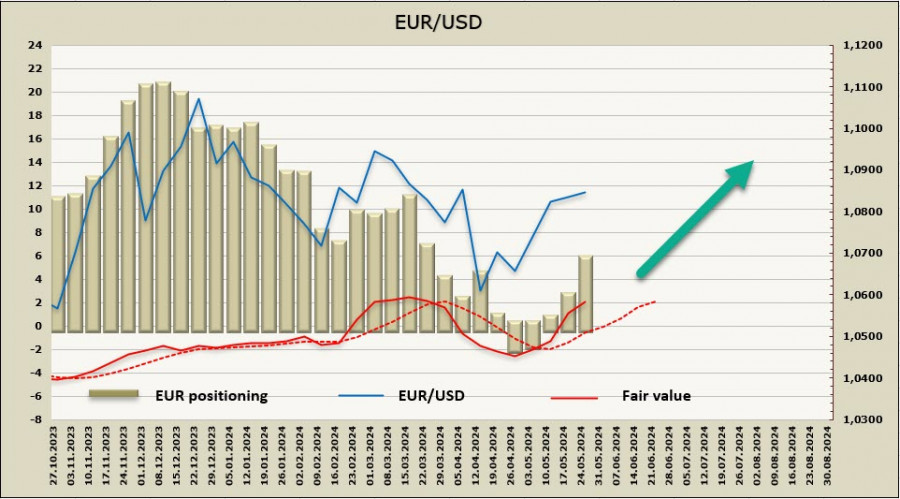

The net long EUR position surged by $3.3 billion week to $5.6 billion over the reporting, shifting from neutral to a bullish position. The price is above the long-term average and continues to rise.

The EUR/USD pair slightly corrected after a strong rise on May 14-15, finding support in the 1.0800/20 zone. We expect the uptrend to resume with 1.0970/80 as the target. The likelihood of a deeper pullback to 1.0700/20 is low, as the bullish momentum is gaining strength.

The material has been provided by InstaForex Company - www.instaforex.com #

Download NOW!

Download NOW!

No comments:

Post a Comment