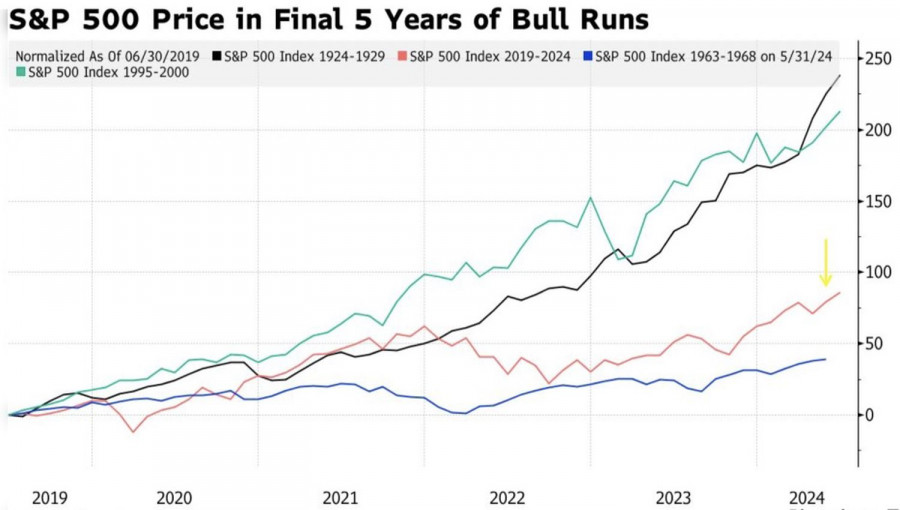

S&P 500 Dynamics in Bull Markets

According to Deutsche Bank, the corporate profits of the companies included in the S&P 500 grew 13% above Wall Street consensus estimates in April-June. This marks the sixth consecutive quarter in which the indicator has exceeded average forecasts, which is excellent news for bulls of the broad stock index. However, to understand the factors driving its northern march, one must examine the structure.

In the 1970s, the share of industrial enterprises and material suppliers was 26%; now, it has decreased to 10.6%. In contrast, the weight of technology and finance has grown from 13% to 42% over the same period. The technology sector alone accounts for 29%, with 6 of the 7 largest corporations by market capitalization belonging to this sector.

This means that the modern S&P 500 is more sensitive to artificial intelligence and interest rates than to the health of the US economy and corporate profits. It's no surprise that shares of AI-related companies increased their value by 14.7% in the second quarter while others lost 1.2%.

When the market is heightenedly sensitive to interest rates, bad news from the US economy becomes good news for it. Under such conditions, the likelihood of the Fed beginning monetary policy easing soon increases. Indeed, after investors saw disappointing statistics on foreign trade, business activity in the services sector, unemployment claims, and ADP private sector employment, the chances of a federal funds rate cut in September jumped from 63% to 73%. How could the S&P 500 not rise?

If the stock market depends so heavily on rates, reducing the scale of monetary expansion should lead to a faster decline in tech sector stocks compared to others. This is what happened in April.

P/E Dynamics by Sectors of the US Stock Market

With two Fed rate cuts in 2024 and three to four in 2025, the S&P 500 and its dominant tech sector are destined to continue rallying. The main thing is that the US economy does not collapse into a recession.

Technically, on the daily chart, the S&P 500 has finally reached the previously set target for long positions at 5535. As long as the broad stock index trades above its fair value of 5465, bears continue to dominate the market. Use pullbacks to form long positions towards 5650 and 5800.Pentru mai multe detalii, va invitam sa vizitati stirea originala.

Download NOW!

Download NOW!

No comments:

Post a Comment