If the economy is strong, won't inflation start accelerating again? Especially since the Federal Reserve's 50 basis point rate cut at the start of the cycle has made financial conditions more conducive to price growth. Such thoughts crossed investors' minds after EUR/USD failed to stay above the 1.12 mark. The US dollar was massively sold off following the September FOMC meeting; however, the euro has too many vulnerabilities to seriously count on a strong rally.

Fed Chair Jerome Powell's assurances that the American economy is strong and that the aggressive start of the Fed's monetary easing cycle is aimed at supporting it have led to an increase in global risk appetite. High-yield currencies became favorites. In particular, the New Zealand and Australian dollars have been performing the best after the Fed meeting. The worst performers have been low-yield currencies like the yen and the franc. Investors are ready to return to carry-trade, which puts some pressure on the euro. After all, it is not easy to classify this currency as profitable.

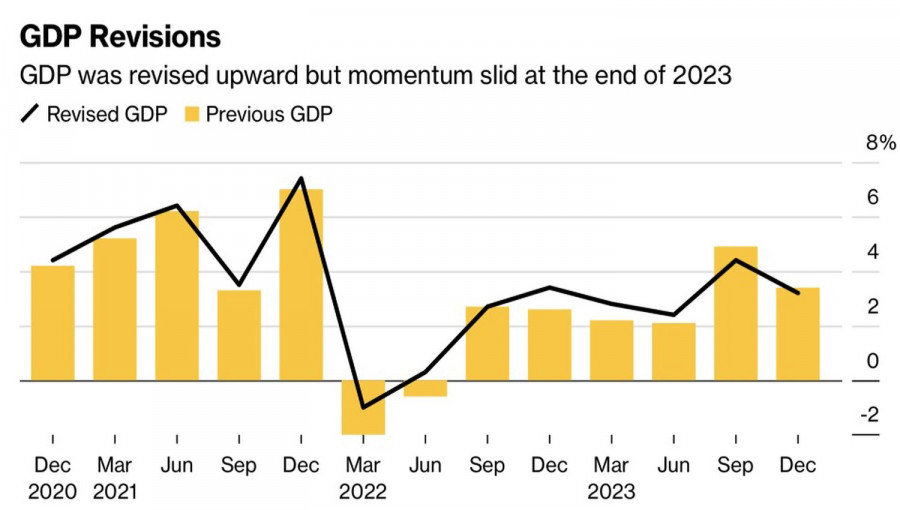

Strong US data is fueling the fire. Unemployment claims have fallen to a four-month low, indicating a strong labor market. Durable goods orders exceeded Bloomberg experts' forecasts. US GDP growth for the first quarter was revised from 1.4% to 1.6%, and it remained at 3% in the second quarter. Overall, in the five years up to 2023, the figure increased by $294.2 billion more than initially estimated.

The Dynamics of the US Economy

The stronger the economy, the more likely it is to withstand the Fed's monetary restriction, even as serious as in 2022-2023. Unsurprisingly, the latest data does not indicate an imminent recession. The chances of a soft landing are high, which means inflation might get a second chance, just like in January-March, when the Fed had to revert to hawkish rhetoric after the dovish pivot at the end of 2023. Hopefully, the 50 bps cut in the federal funds rate in September won't turn out to be a mistake.

Meanwhile, the euro is facing challenges due to rising political risks. For the first time since 2007, the yield on French bonds has fallen below that of their Spanish counterparts. This might seem unalarming at first glance, but Madrid has a lower rating than Paris, so the yield spread dropping below zero signals serious problems in France.

The Dynamics of the Yield Spread Between Spanish and French Bonds

Thus, the market is in a tug-of-war. On one hand, the start of the Fed's monetary easing cycle provides solid grounds to get rid of the US dollar. On the other hand, the euro has too many vulnerabilities, and US inflation could return.

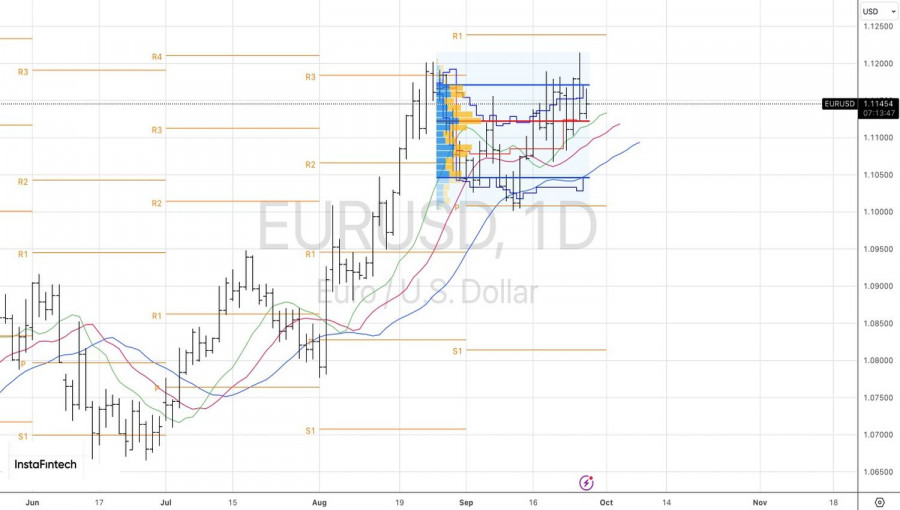

Technically, on the EUR/USD daily chart, uncertainty manifests as an inside bar. Using pending buy orders from 1.1165 and sell orders from 1.1120 makes sense.

The material has been provided by InstaForex Company - www.instaforex.com #

Download NOW!

Download NOW!

No comments:

Post a Comment