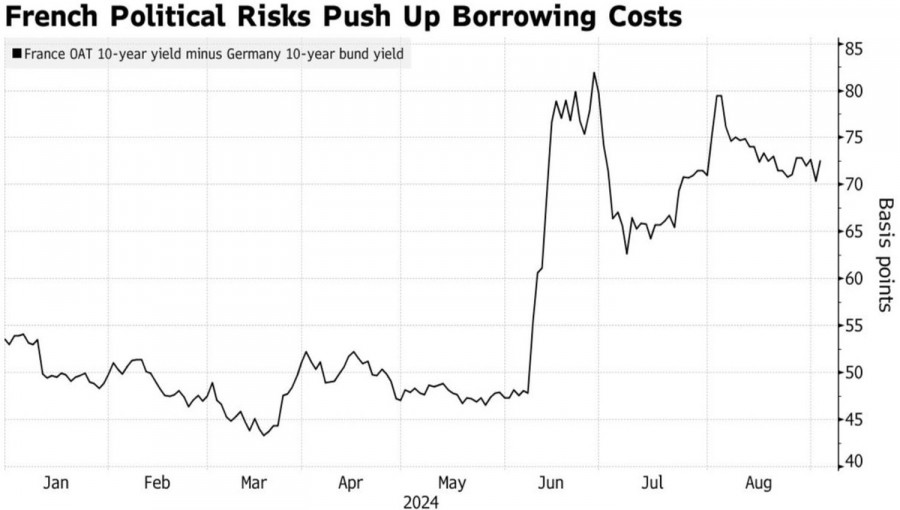

When your opponent is openly weak, your vulnerabilities go unnoticed. But as soon as they rise from their knees, the sore spots start to make themselves felt. Amid the rapid EUR/USD rally in August, few remembered that France still has no government. In France, protests call for Emmanuel Macron to resign, and the widening yield spreads between local and German bonds indicate an increase in political risks. This spells trouble for the euro.

Dynamics of the Yield Differential Between French and German Bonds

The situation in Germany is no better. Its GDP has fallen in three of the last five quarters, and indicators of business activity, business climate, and consumer confidence signal a crisis. Moreover, nationalists are winning local elections. To make matters worse, failing to agree with trade unions on wages, Volkswagen is shutting down German factories for the first time in its history. Combined with the economic weakness of China and the US, which is a clear negative for export-oriented Germany, it becomes evident that the situation is dire.

Surprisingly, MUFG forecasts a transition for EUR/USD into a trading range of 1.10–1.15, based on the markets' expectations of aggressive monetary easing by the Federal Reserve and a recovery in the Eurozone economy. The main risks include the US presidential elections, global trade uncertainty, and China's economic weakness. ING believes the yield spread between U.S. and German bonds will support the euro at the $1.10 level.

Thus, banks consider the decline in EUR/USD quotes at the end of summer and the beginning of autumn as a technical correction and continue to believe in the recovery of the upward trend. However, the correction of the main currency pair may continue, as the European Central Bank seems poised to lower its deposit rate in September.

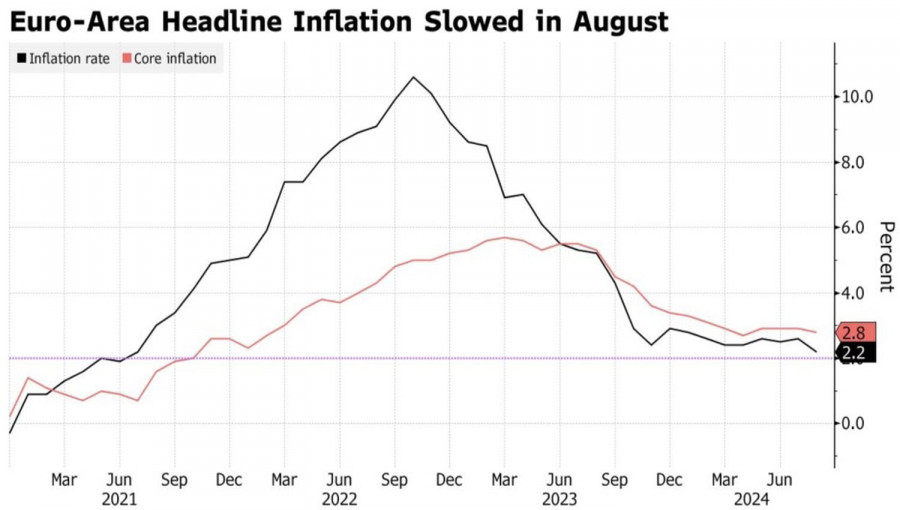

Dynamics of European Inflation

According to ECB Governing Council member Pierre Chipollone, the central bank cannot maintain borrowing costs at the current high level for too long, as it would harm the economy. Monetary policy risks becoming too restrictive. Even Bundesbank President Joachim Nagel, who is a hawk, believes that inflation is on the right track. He is prepared to vote for easing monetary policy in September if convinced by the data.

Thus, the political crisis in France and Germany, the weak stance of the German economy, and the ECB's readiness to continue the rate-cut cycle in September are putting pressure on the euro. At the same time, the reassessment of market views on the fate of the federal funds rate supports the US dollar. The correction of the main currency pair appears justified.

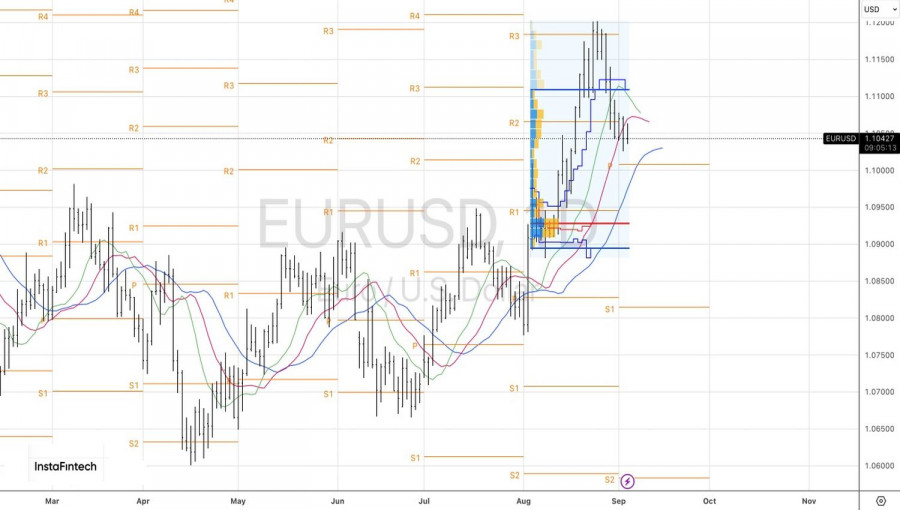

An inside bar may be forming on the EUR/USD daily chart. The chances of breaking through the support at 1.1035 are quite high, which would justify new sales—likewise, a rebound from the resistances at 1.107 and 1.111.

The material has been provided by InstaForex Company - www.instaforex.com #

Download NOW!

Download NOW!

No comments:

Post a Comment