The euro reacted modestly to slight improvements in the Eurozone PMIs. Despite the small growth in the indicators, it is not yet appropriate to speak of a recovery in activity, only of its less active contraction. Against this backdrop, a recession in the Eurozone seems much more likely, and whether a larger economic downturn can be avoided in the fourth quarter of this year is a rather rhetorical question.

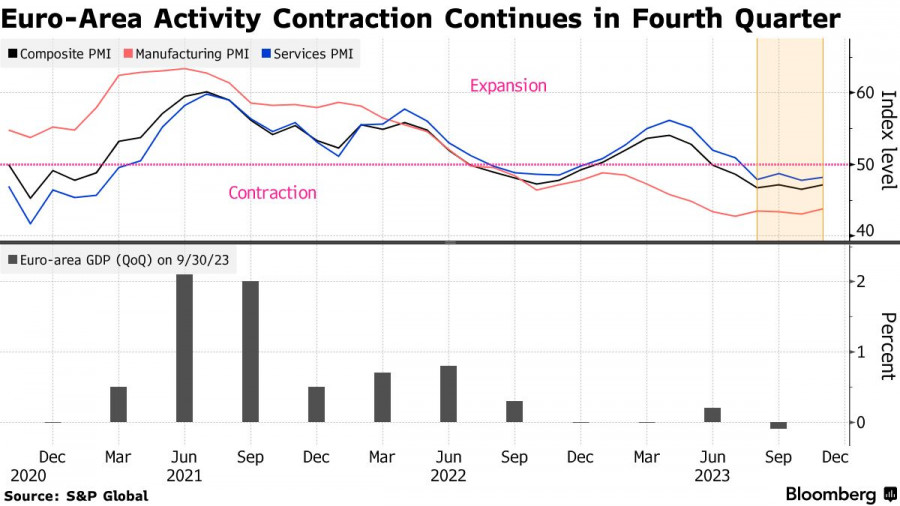

As the data showed, the S&P Global Purchasing Managers' Index (PMI) in November again decreased, reaching a mark of 47.1 points, although it was slightly higher than economists expected. The index has been below the 50 level, which separates growth from contraction in activity, for the sixth consecutive month. Both the manufacturing and services sectors showed a similar trend.

It is evident that the Eurozone economy is stuck in the mud, and recent data indicate the potential for a GDP contraction for the second consecutive quarter. After a 0.1% decline in gross domestic product in the third quarter, today's data indicate a similar, if not worse, situation awaiting the Eurozone economy in the fourth quarter. The above figures also sharply contrast with the European Commission's forecast of a return to growth and analysts' expectations of stagnation in this quarter.

Recent warnings from European Central Bank Vice President Luis de Guindos that the markets may not fully factor in the risk of a stronger blow to the Eurozone economy after a year of interest rate hikes and increased political tension are evidence that not everyone is looking at the situation through rose-colored glasses. He also cautions the market against mistaking the desired for the real.

The report indicates that the two leading economies in the region found themselves in the grip of significant weakness, although Germany's PMI data for November shows a slightly better situation than in France. The activity decline in Germany slowed down in November, signaling that growth will return to the Eurozone's largest economy after a likely recession this year. In France, the S&P Global Supply Managers' Index practically remained unchanged at 44.5 points.

The S&P Global report also notes that private sector activity declined more slowly than in the previous month and less than economists expected. Conditions improved in both manufacturing and services, with the number of new orders showing a moderate contraction.

Some believe that the Eurozone GDP will remain unchanged in the fourth quarter of this year. However, according to ECB economists' forecasts, many models indicate the danger of a repeat production contraction. Economists expect GDP growth of 0.1%.

EURUSD's technical picture shows that buyers need to stay above 1.0890 to maintain control, which will allow breaking through to 1.0925 and 1.0970. From this level, it is possible to climb to 1.1005, but doing so without support from major players will be quite problematic. The ultimate target will be the high of 1.1400. In the case of a decline in the trading instrument, I only expect significant actions from major buyers around 1.0890. If there is no one there, it would be good to wait for a retest of the low at 1.0860 or open long positions from 1.0830.

As for GBPUSD, demand for the pound remains. It will be possible to count on further strengthening of the pair only after gaining control over the level of 1.2525. Consolidation in this range will revive hopes for recovery towards 1.2560 and 1.2600, after which it will be possible to talk about a more pronounced upward surge towards 1.2630. In the event of a pair's decline, bears will try to take control at 1.2525. If they succeed, a breakdown of the range will strike a blow to bullish positions and push GBPUSD towards the low of 1.2485 with the prospect of reaching 1.2450.

Download NOW!

Download NOW!

No comments:

Post a Comment