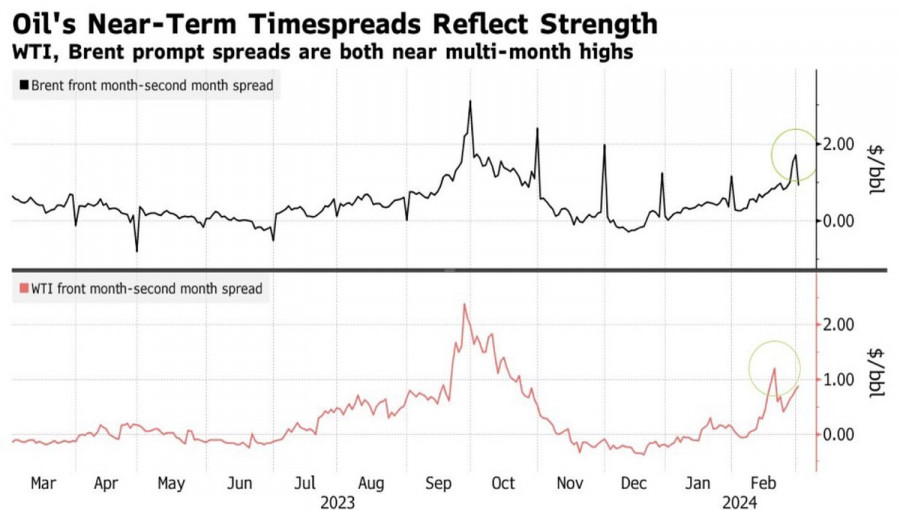

The most significant burden falls on Saudi Arabia, producing 2 million bpd less than in November 2022. OPEC+ collectively produces 5.3 million bpd less, which accounts for 5% of global production, inevitably impacting Brent. Since the beginning of the year, the North Sea crude has risen by 7%, partly due to non-OPEC producers not rushing to fill the void in the market, as they did in 2023. As a result, spreads between nearby contracts expand to 4-month highs, and the oil market becomes increasingly bullish.

Spread dynamics for Brent and WTI

Support is driven by the belief that the global economy may grow faster than anticipated at the end of 2023. This would boost global demand, especially considering that China, the world's largest oil consumer, has set an ambitious GDP target of +5% for 2024. Achieving this goal would require additional fiscal and monetary incentives, theoretically creating a tailwind for Brent. However, Bloomberg experts believe the target is overstated, suggesting that the economy will expand at best by 4.6%.

The strong U.S. dollar is exerting pressure on the North Sea crude. Federal Reserve Chairman Jerome Powell is expected to emphasize the need to maintain the federal funds rate at 5.5%, at least until the second half of 2024, in his Congressional testimony. This will not please Democrats who would prefer to avoid economic cooling due to high borrowing costs. However, the risks of inflation force the Fed to be cautious.

Oil volatility dynamics

Meanwhile, speculators, amid decreasing volatility, are shifting from the bear camp to the bull camp. By the week ending on February 27, they increased long positions in six major oil and oil product benchmarks by 10 million barrels equivalent. In eight out of the last 11 five-day periods, fund managers have been acquiring oil. As a result, net longs grew to 532 million barrels.

Technically, on the daily chart, the bears managed to win back the internal bar, but the bullish bias persists. In conditions of falling volatility, it makes sense to bet on the uptrend and buy the North Sea grade on bounces from dynamic supports, such as moving averages and the pivot level at $81.55. Returning above the fair value at $82.9 and above the high of the inside bar at $84.05 should also be considered as a signal to form or increase long positions.Pentru mai multe detalii, va invitam sa vizitati stirea originala.

Download NOW!

Download NOW!

No comments:

Post a Comment