And the last shall be first. From the ugly duckling or main underdog of the international currency market, the Japanese yen suddenly transformed into a beautiful swan, or the main favorite. The USD/JPY crash from July's low levels reached 13%, and only the calm rhetoric of Federal Reserve officials managed to cool the ardor of the rampant bears. But for how long?

If the break in the ascending trend was due to currency interventions by the Japanese government at just the right moment amid slowing U.S. inflation, other events became the main drivers of the USD/JPY's plunge. At the end of July, the Bank of Japan appeared before investors in the plumage of a hawk. It not only raised the overnight rate to 0.25% and promised to halve the scale of quantity easing by 2026 but also spoke at length about the harm of a weak yen. Previously, central bank heads did not link their verdicts to the currency rate.

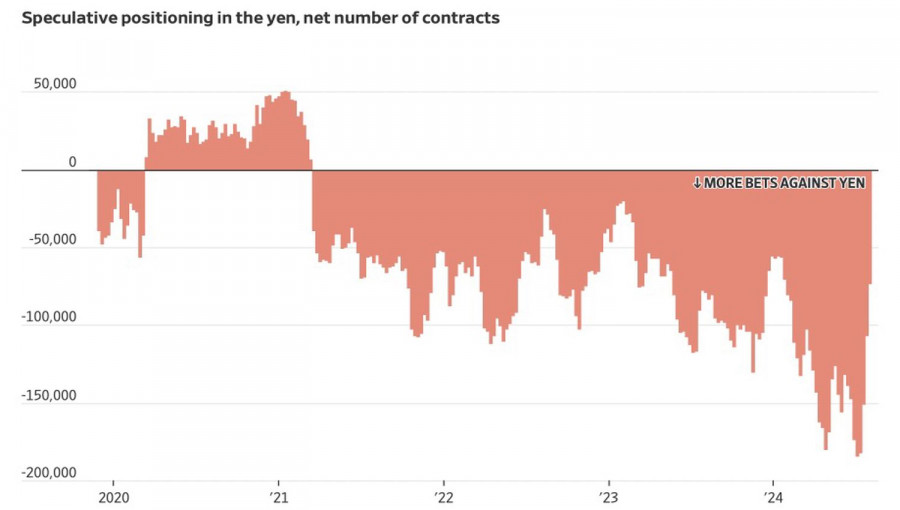

The dismal July data on American employment led to demands for the Fed to aggressively lower the federal funds rate. The futures market estimates the scale of monetary easing at 125 bps in 2024, and the divergence in monetary policy allows hedge funds and asset managers to reduce short positions on the yen. Not long ago, they reached the highest level since 2007, but by the beginning of August, they had significantly thinned out.

Dynamics of speculative positions on the yen

The BOJ has deprived investors of practically free resources by steering towards normalization. Coupled with fears of an American recession and the associated spike in volatility, this has led to the closure of carry-trade transactions. The primary beneficiary has been the yen as a cheap funding currency.

Will the bears' trump cards for USD/JPY continue to work? Moody's notes that the global economy's weakness forced the BOJ to roll back the recently increased rates in 2000 and 2006. It is quite possible that the central bank might do this now, especially if the US actually plunges into a recession. Moreover, the BOJ is facing considerable criticism. How could it ignore the weak data from Japan if it follows a data-dependent policy?

If BOJ Governor Kazuo Ueda and his colleagues take currency exchange rates into account, they are unlikely to rush the continuation of the normalization cycle. It is not certain that the weak US labor market data for July will compel the Fed to cut the federal funds rate aggressively. It seems that the divergence in monetary policy is already priced into the USD/JPY quotes, which lays the groundwork for a pullback.

On the other hand, demand for the yen will be high due to Japanese investors returning to hedge currency risks and further unwinding carry-trade transactions.

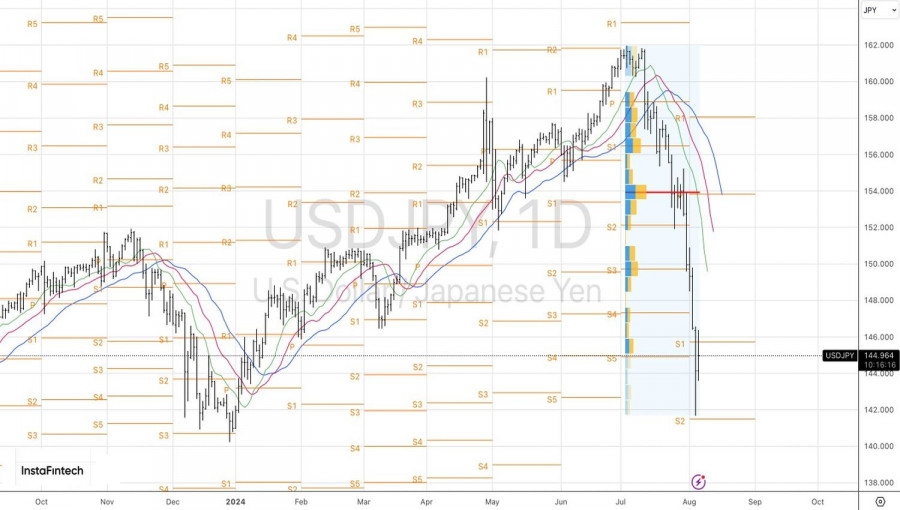

Technically, on the USD/JPY daily chart, the formation of a dead cat bounce is not ruled out. A return above 145.8 would be grounds for taking profits on short positions formed from 153.8 and a reason for long positions in the short term. As long as the pair trades lower, it makes sense to hold positions.

The material has been provided by InstaForex Company - www.instaforex.com #

Download NOW!

Download NOW!

No comments:

Post a Comment